The shifting energy mix and what it means

India is one of the largest producer and consumer of power

The energy mix in India is one of the most diversified in the world comprising of both renewable and non-renewable sources. It includes, Coal, Lignite, Natural Gas, Oil, Hydro,Nuclear, Wind, Solar andBio-fuel. Electricity demand in the country has increased rapidly in the last two decades presently constituting about 5.9% of total global power generation.

"India – Third largest Producer and Consumer in the world next only to US and China"

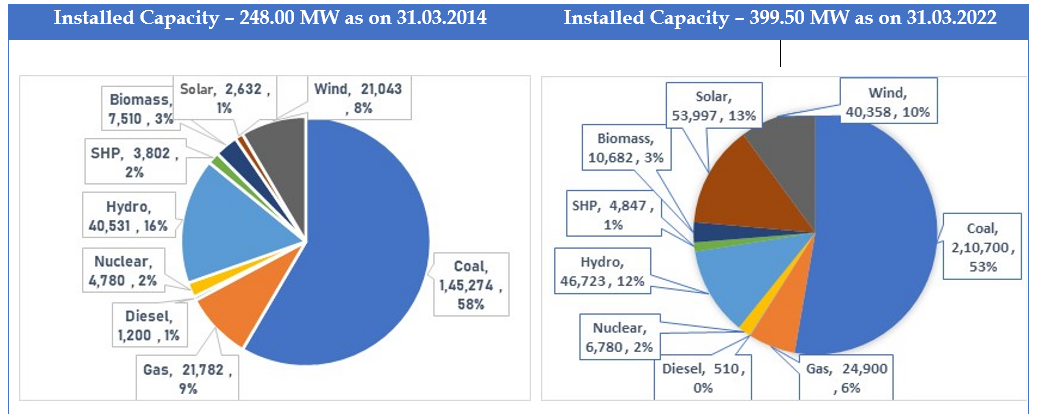

The total installed capacity was 399.50 GW as on 31.03.2022, out of which 236.11 GW is fossil fuel based (Coal/gas etc.) and 163.39 GW is non-fossil fuel (Renewable Energy + Nuclear) based. India is exporting power to Nepal, Bangladesh and Myanmar.

The Shifting Energy Mix

The installed capacity jumped by 60% compared to 31.03.2014 in 8 years, due to increased demand. But the catchy fact is the decrease in non-renewable and increase in renewable component.

Source: Ministry of Power

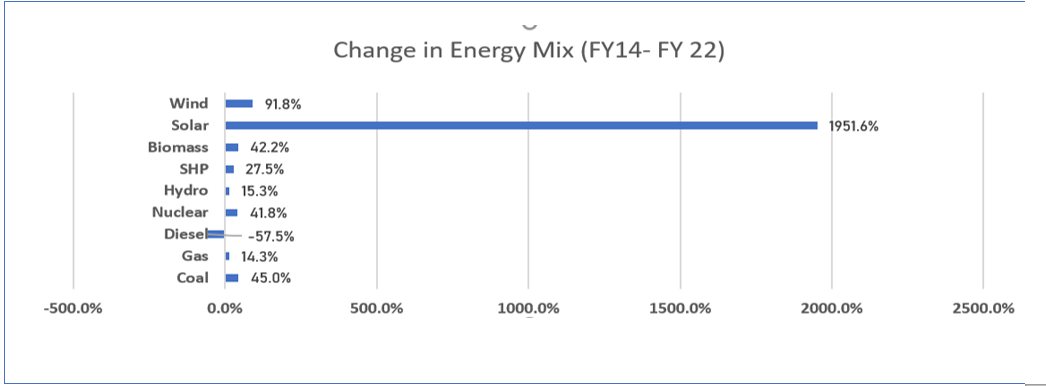

The increase in the capacity of Solar power generation jumped from 2,632 MW in FY 14 to 53,997 MW i.e., an increase of 1,950%. The second highest increase is noticed in the Wind power capacity, which increased by 92% in 8 years. In the absolute term, the addition in the capacity of coal -based power plant increased by 65,426 MW, which is much higher than the addition of Solar power capacity, the ground is set for exponential increase in the renewable generation.

Renewable Energy Sources and India’s Commitment

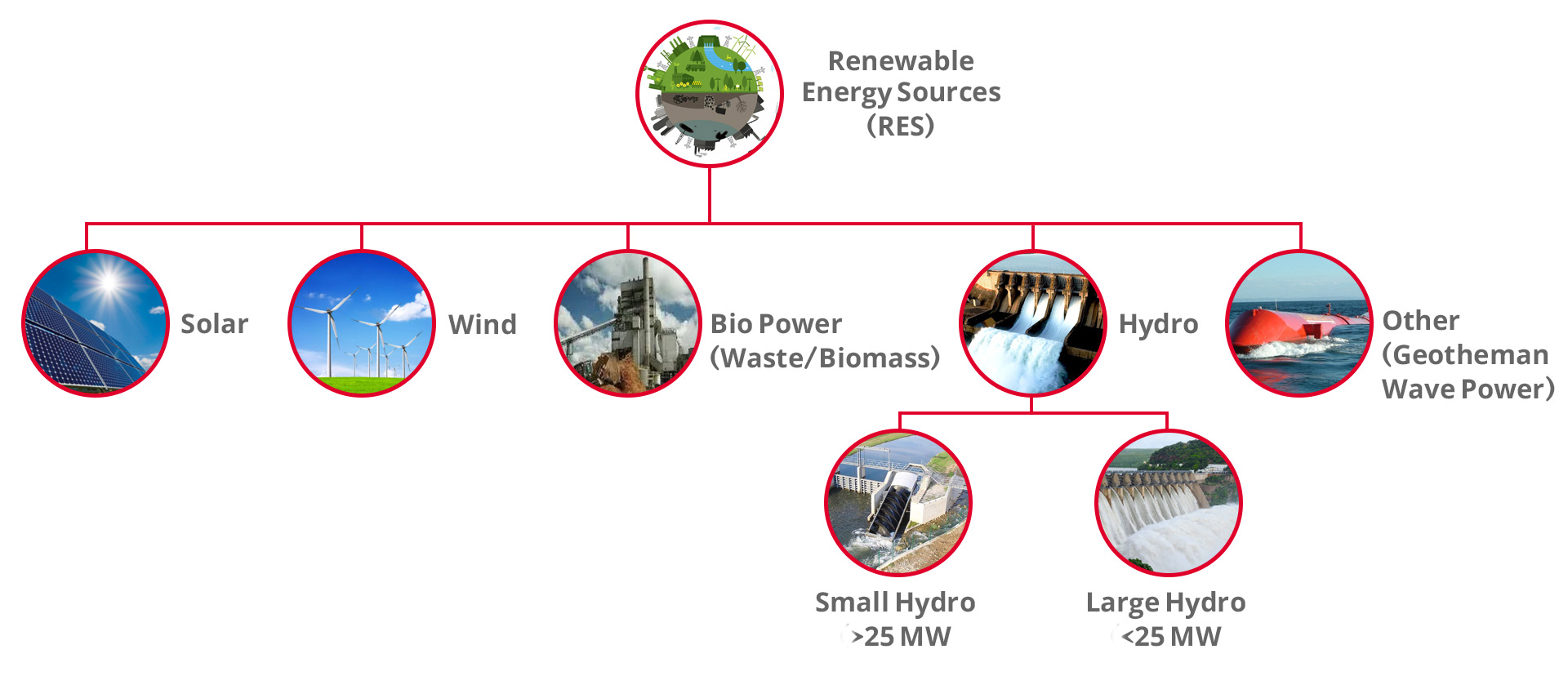

The Renewable Energy sources are defined by the nature of its energy source, which is replenished naturally or there is an enormous source of continuously emanating energy.

The fact that they are non-polluting, i.e., they do not produce harmful gasses or cause any other kind of pollution during its operational phase, make them different from conventional non-renewable energy sources.

India is the only country among the G20 nations that is on track to achieve the targets under COP 26 are reasonably high and challenging targets. It targets to achieve

| - 500 GW of renewable power by 2030 - 50% of total energy requirement from renewable power by 2030 - Reduction total carbon emission by 1 billion MT by 2030 |

Within renewable sector, Solar sector has picked up very rapidly with close to addition of 13 GW of Solar PV in 2021 alone. India is the second largest market in Asia for new Solar PV capacity and third globally.

Government Support

Solar energy has taken a central place in India's National Action Plan on Climate Change with National Solar Mission (NSM) as one of the key initiatives. NSM is a major initiative of the Government of India with active participation from States to promote ecological sustainable growth while addressing India’s energy security. It also is a major initiative in India’s effort to meet the challenges of climate change.

In order to achieve the targets, the Government of India has launched various schemes to encourage generation of Solar power in the country like, Solar Park Scheme, VGF Schemes, CPSU Scheme, Defence Scheme, Canal bank & Canal top Scheme, Bundling Scheme, Grid Connected Solar Rooftop Scheme etc.

Various policy measures undertaken included declaration of trajectory for Renewable Purchase Obligation (RPO) including Solar, Waiver of Inter State Transmission System (ISTS) charges and losses for inter-state sale of Solar and Wind power for projects to be commissioned up to March 2022, Guidelines for procurement of Solar power though tariff based competitive bidding, Standards for deployment of Solar Photovoltaic systems and devices, Provision of roof top Solar and Guidelines for development of smart cities, Amendments in building bye-laws for mandatory provision of roof top Solar for new construction or higher Floor Area Ratio, Infrastructure status for Solar projects, Raising tax free Solar bonds, Providing long tenor loans from multi-lateral agencies, etc.

Recently, India achieved 5th global position in Solar power deployment surpassing Italy. Solar power capacity has increased by more than 21 times in the last five years from 2.6 GW in March,2014 to 54 GW in March 2022. Presently, Solar tariff in India is very competitive and has achieved grid parity.

Ambitious Target for FY 30

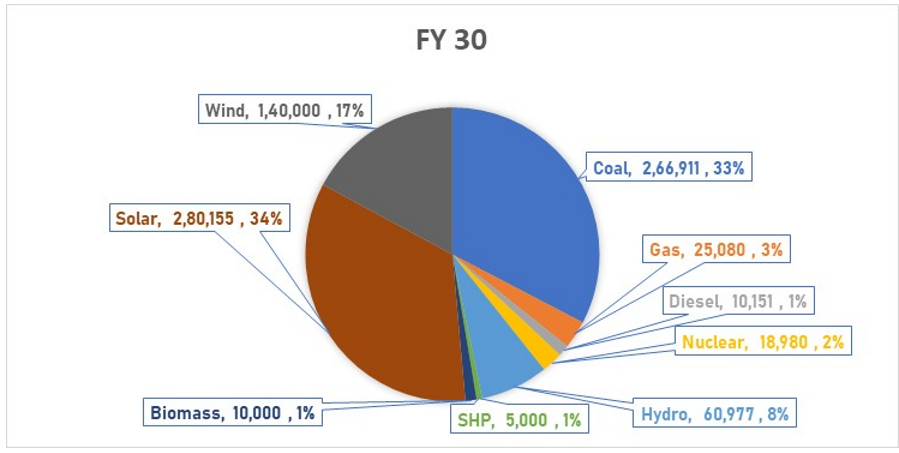

The growth targets in the sector are steeper than it has achieved in the preceding 8 years span. The Country plans to achieve 280 GW of Solar and 140 GW of Wind generation capacity by 2030, which is an increase of 420% in Solar and 250% in Wind capacity compared to March 2022 figures. Though, substantial capacity is planned to be added in thermal power sector too, the increase is merely 27% over March 2022 figure.

Source : CEA

Though the targets are considerably challenging, it is expected that the entire economy and the support infrastructure will attempt to achieve the most.

What It Means?

There are different take-aways for different stakeholders and the perceivable outcome as believed by Adroit Advisors are as follows,

- There will be faster dismantling of end of use & highly polluting Thermal Power Plants in the country. The pollution control norms are slowly becoming more stringent, which is making the older generation thermal power plants un-sustainable. Over and above the cost of operation of these plants are considerably higher in view of poor efficiency issues.

- The planned capacity expansion may require Rs. 11 Trillion for Solar sector and Rs. 5 Trillion for wind sector between FY 2022-30. The expected investment requirement in the Thermal power sector is expected to be at a much lower extent of Rs. 2.25 Trillion.

- There may be increased efforts in consuming Biomass in power plants to, (i) reduce exploration/ import of coal and (ii) minimize the environmental pollution caused due to uncontrolled stubble/ biomass burning, primarily in Northern India. The experimental use of stubble in the power plants is already in progress.

- The sustainability concerns of Thermal power plants may drive investors away from their exposure in the sector. It may also lead to increased interest rate making it a deterrent towards investment.

- In the long run the cost of Renewable Energy will be much more competitive, allowing increased installation of Solar modules by private individuals. Additionally, the intention to be environmentally aware will influence many individual users.